On 1 September Discrepancy Reporting comes into operation. A new section 70000 has just been added to TRSM. 70040 introduces a new proof of registration document. In particular it must contain:

“5. This statement:

This document confirms that the trust named below has been registered on the Trust Registration Service in the United Kingdom. Details of the beneficial owners of the trust as held on the register are shown below”.

I have pdfs of my registered trusts which HMRC’s system entitles " Last declared copy of the trust’s registration" to which I have had to add the trust’s name. As far as I can see this document is non-compliant and furthermore there must be a “4. Date of issue”, implying that this will be an HMRC-generated document.

It is not a problem for existing trust clients only for new clients where a business relationship of some duration is expected but the "relevant person " cannot act without having a statement for such new clients.

I cannot see any HMRC guidance on obtaining these statements although the new Reg 30A (in Reg 5 of SI 2020/991) has been published since September 2020!. TRSM bandies about profusely the term “proof of registration document” but says nothing about how a trustee is to acquire one unless it is the saved pdf that I have.

Can anyone shed any light, especially those who have unacceptable inside knowledge from their clandestine cadres of the Great and the Good with privileged access to the communications or even the metaphysical or telepathic thought processes of our Magnificent Tax Authority?

Trust and Estates Newsletter August 2022 “The trustee or agent who is engaging in the business relationship will need to use the online service to download a PDF copy of a report to show proof of registration. This report can be emailed to the relevant person or alternatively, can be printed off”.

I am sure this publication is compulsory reading for every trustee and that the heading “reporting a discrepancy” would immediately alert them to the issue.

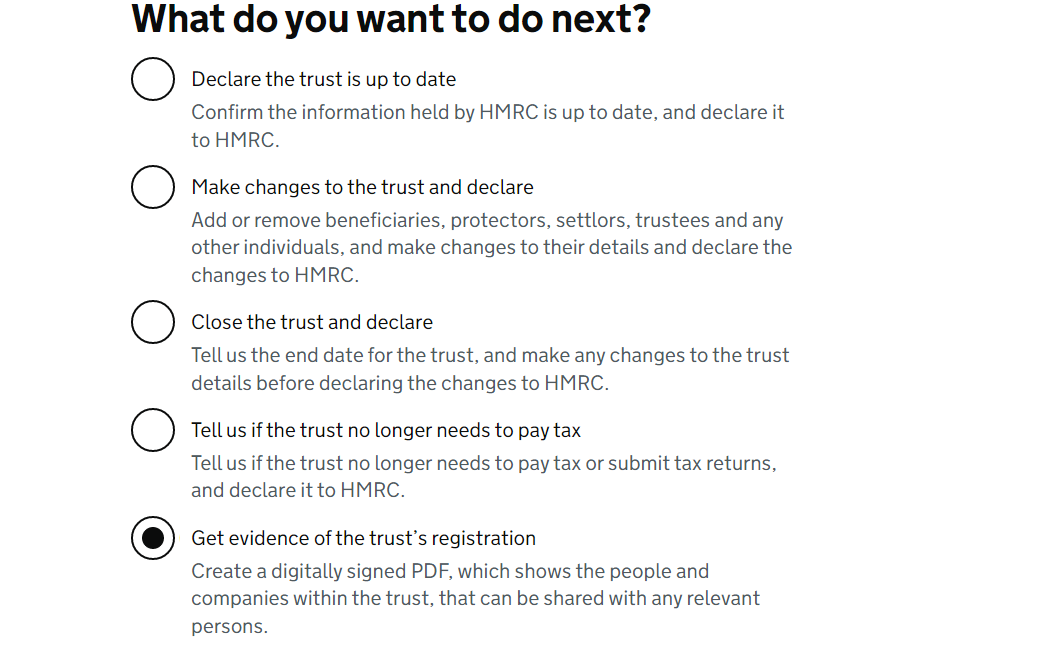

I think (but haven’t tried recently) that if you log onto the TRS system and go to the particular client you can print off a proof of registration document.

Privacy Notice - details of our legal basis for processing your information, retention period for data held, security of your data, your rights under the General Data Protection Regulations (GDPR) including the right to complain can be found in our full Privacy notice

This email and the information contained in it and in any attachments are confidential and may be privileged. If you have received this email in error please notify us immediately. If you are not the intended recipient, you are not authorized to, and must not use, disclose, copy, distribute, retain or rely on this email or any part of it.

Please note that whilst we try to ensure that attachments are virus-free, we cannot accept responsibility for situations where this is not the case.

Any information in this email is advice from the business and not the sender.

Sara Spencer Ltd is a company registered in England, registration number 12304408, registered office 8 Kingsway, Harrogate, HG1 5NQ

As the agent can only access TRS to obtain this document after the business relationship has begun, and cannot act e.g be authorised as agent until it has been obtained, it would seem that the trustee must obtain it. Surely this merits a specific comment in guidance?

This produces a PDF that looks like a letter from HMRC, rather than a screen print.

You are right that the trustee (or current agent) would send that to the new agent, or whoever the business relationship is with. The wording in the guidance at TRSM70000+ isn’t great.

As an aside, the guidance suggests that if there is a discrepancy, or the trust has not registered, you cannot act UNTIL this is fixed.

“If appropriate, Relevant Persons should request that the trustee/agent update TRS / register the trust prior to the commencement of a Business Relationship” TRSM70010

However I would have thought that if a trustee wanted assistance we can assist with the registration as the “first job”. The same as if a person had not registered with HMRC for SA and was behind, we’d get them registered.

Otherwise the trustee (who may not understand any of this) won’t ever be able to get help to bring the trust up to date.

Jack, do you read the guidance/rules this way, or would you read it as you can assist to bring them up to date? I prefer the latter, and would go down that route to be honest.

Further to my post HMRC has confirmed on the agent forum

It is consistent with the aims of the MLR and HMRC guidance, that, where it is within their professional ability, a relevant person may resolve the issue of a trust not being registered by either registering that trust or assisting them in the registration process.

There is no requirement for the relevant person to report, or cease engagement with, any Trust that they are in the process of registering.

I have just instructed an agent to manage my trusts’ TRS matters because, to the chagrin of some but joy of others, I am not immortal (unlike, apparently, many of my former clients). I told them they would need these proofs and downloaded them ahead of their engagement letter. As HMRC apparently insist that the trustee must claim the trust first anyway a typical lay trustee may need some help with guidance even on how to register. Even an organisation as congenitally obtuse as HMRC is unlikely to pursue an agent who restricted the initial contact to drawing attention to its own guidance on how to register. Advising on whether to register is a step further but possibly not too far. “Establishing a business relationship” is a long standing AML concept and CDD requires a risk-based approach. What would the risk be here? An agent should pay heed to his own professional AML guidelines of course.

When in practice I was an implacable enemy of AML but aware of the need for self-preservation. I tried to apply common sense and sometimes the conscience of a well-trained hippopotamus. A difficult occasion was always when a prospective client was suspected of evasion or admitted it (the facts if not the characterisation!). AML allowed me in my view to warn them of the possible consequences, avoiding tipping off, and that I could not act without their having a “firm purpose of amendment” and a commitment to full disclosure. Up to this point I think no business relationship had been established.

So I would be prepared to advise a prospective new client if necessary that the trust needed to be registered, how to do that and obtain the proof of registration, and would say that I could not advise further until that was provided. I am only sorry that I cannot now be a test case if HMRC want to have a pop at someone for assisting them in their statutory duty of ensuring compliance with the law.

My above post confirms you can register the trust on their behalf or assist them in doing so.

Obviously that has to be first thing to do or you may get in “trouble” if you do other work before they are registered.

I’ve generated one of these proofs for a taxable trust.

It gives for the settlor, trustees and beneficiaries in the boxes next to the ones marked “Date of Birth” merely the month and year of birth. Reg 45(6)(e) requires the date of birth to be supplied for individual BOs. How would a relevant person know if there was any discrepancy between the information it holds relating to dates of birth to the register entry? I would seem that a RP would also need a copy of the most recent declaration.

NB for non-taxable trusts Reg 45ZA(3)(a)(ii) requires only the month and year of birth (if the trust has not previously been a taxable trust).

The settlor is also a trustee and under settlor it has his first and last names and under trustee it has his first, middle and last names. This might be because the field for middle name has “(optional)” after the word '“middle” and there may have been some inconstancy by the inputter. Both Reg 45 and 45ZA require full names so the word optional is really odd. Perhaps HMRC mean ‘leave blank if no middle name’. If so, why not say leave blank?

I add, if registering a non-taxable trust, you answer the question “do you know X’s date of birth?” truthfully in the affirmative you have no choice but to give the full DoB even though the law only requires the month and year.

Personally if they provide that TRS generated letter that is, in my view, enough to engage the client as it proves the trust is registered.

Once you get access to the actual TRS you can see the full details.

Middle name issues, I’d just update it to include the full name once I have access. I expect this can be classed a “minor” error.